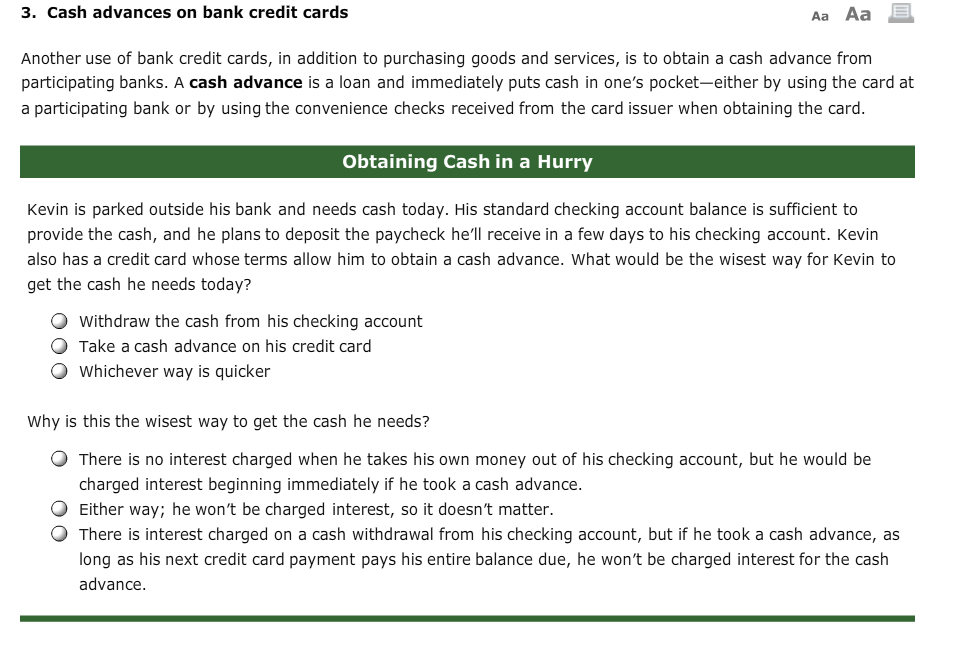

The benefits and Cons off a property Security Line of credit (HELOC)

paydayloanalabama.com+midfield payday loan instant funding no credit checkA house guarantee credit line, otherwise HELOC should be a good option to invest in a primary lifetime expenses including a home repair , combine loans otherwise safety an urgent situation.

While you are there’s high advantages of choosing an effective HELOC it provides a noteworthy downside, which is that you have to put your household upwards given that guarantee so you can secure your loan.

What exactly is a home collateral credit line (HELOC)?

A beneficial HELOC is actually a home loan which allows you to definitely tap into your family collateral and you may access bucks in the a relatively lowest interest. HELOCs was revolving credit lines that means much like borrowing cards and invite you to definitely repeatedly take-out currency around their complete line of credit throughout your mark several months (always a decade), the time period whenever you generate withdrawals out of your HELOC.

- At the very least 15% to help you 20% guarantee gathered of your house

- Good credit (really loan providers prefer a score of at least 700 so you can approve you due to their lowest prices, you could meet the requirements with a rating only 620 with a few lenders)

- proven earnings

- A debt-to-earnings ratio that’s 43% or less

Positives of an excellent HELOC

HELOCs are apt to have down rates of interest than many other type of funds since they’re safeguarded by the household. As you takes away money as needed more an effective ten-year months, HELOCs can be helpful when you need money for some time-term opportunity however, commonly clear on the actual matter need.

Low interest rates

HELOCs usually have down rates than other house equity finance, unsecured loans otherwise credit cards. Protecting a decreased possible interest rate will help help you save 10s of several thousand dollars along the longevity of your loan. Immediately, new federal average HELOC speed is 7.34%, centered on Bankrate, CNET’s sister sitepare that so you can personal loans and therefore actually have an average price from %, for example.

Interest-just repayments

During your mark months, you possibly can make attention-simply repayments in your HELOC, which means you makes minimal monthly obligations for decades, which means that your loan will get a reduced affect their month-to-month budget. And additionally, it’s not necessary to take-all of your own money aside the simultaneously, while pay notice simply into count you have taken perhaps not this new entirety of mortgage, that can helps you to save rather towards the notice.

Very long draw and you may repayment attacks

Being able to constantly take-out money through the a draw period away from a decade is a primary advantageous asset of an effective HELOC especially because you can create focus-simply payments, and do not need to start making costs in your dominating financing harmony until your repayment period starts (that past from five so you’re able to 20 years). You to affords you flexibility in the way you employ the loan, and offer your for you personally to bundle to come toward huge payments you must make when you go into their installment several months.

Disadvantages off a HELOC

Well-known downside to a beneficial HELOC is that you you want to utilize your residence since the security to safe your loan, and that leaves you at risk of foreclosure for those who miss payments otherwise cannot pay your loan for any reason. In the modern ascending interest environment the reality that HELOCs provides varying interest levels is additionally faster useful, as Government Set aside has showed that it does raise appeal cost one longer up until the prevent out-of 2022.

Changeable rates of interest

As opposed to home equity money gold keeps cash-out refinances , which are repaired-interest money, HELOC rates go up and you may fall based on macroeconomic affairs such as inflation and you will employment progress. HELOC pricing was to step three% at the beginning of the entire year but have today surpassed the 7% mark.

Your home is guarantee towards the financing

How come finance companies and loan providers have the ability to present lower interest levels on your HELOC is basically because your residence serves as collateral for the financing. It means its less of a danger to enable them to offer your financing, as they can pay on their own right back by repossessing your residence in the event the you default on the HELOC. Yet not, extremely banking institutions and you will loan providers are often prepared to work with you in order to see a way to back the loan, because it together with benefits them to continue choosing costs from you.

Minimal withdrawals

Though it vary from the financial as well as the particular regards to the loan, of numerous loan providers require you to generate minimal distributions from the HELOC. Which means you will have to pay notice into those funds actually or even find yourself using them, that will charge a fee extra money when you look at the attract through the years.

The conclusion

HELOCs is a handy cure for availableness bucks from the a comparatively low interest. They are useful in affairs if you want money more a beneficial long time, of course you might not know exactly how much cash you need. It’s important to just remember that , the loan is actually covered by your household, meaning that if you miss money or standard in your HELOC, your own financial otherwise bank could repossess your property. It’s crucial to be certain that you’re prepared to manage your credit line obligation and now have room on the cover switching monthly obligations.