So why do Vendors Seem to Dislike Virtual assistant Loans?

advance cash near me- Customer care: How do you contact customer support if you have a concern? Understand the circumstances and exactly how receptive they are. This is certainly a big pick and also you desire to be sure which have whom you’re writing on.

Get a beneficial Va Financing

After you have made the Virtual assistant financing alternatives, make an effort to offer their COE showing your eligible to be eligible for good Va loan. You can buy they using your eBenefits portal or of the requesting it through the mail. 2nd, you will work with that loan administrator and you will over an application, have your credit work on, as well as have pre-qualified for the loan. You’ll need your public security number and you will character and have now may require proof money such an income tax come back. It creates the procedure much easier if you find yourself structured while having every of your records useful.

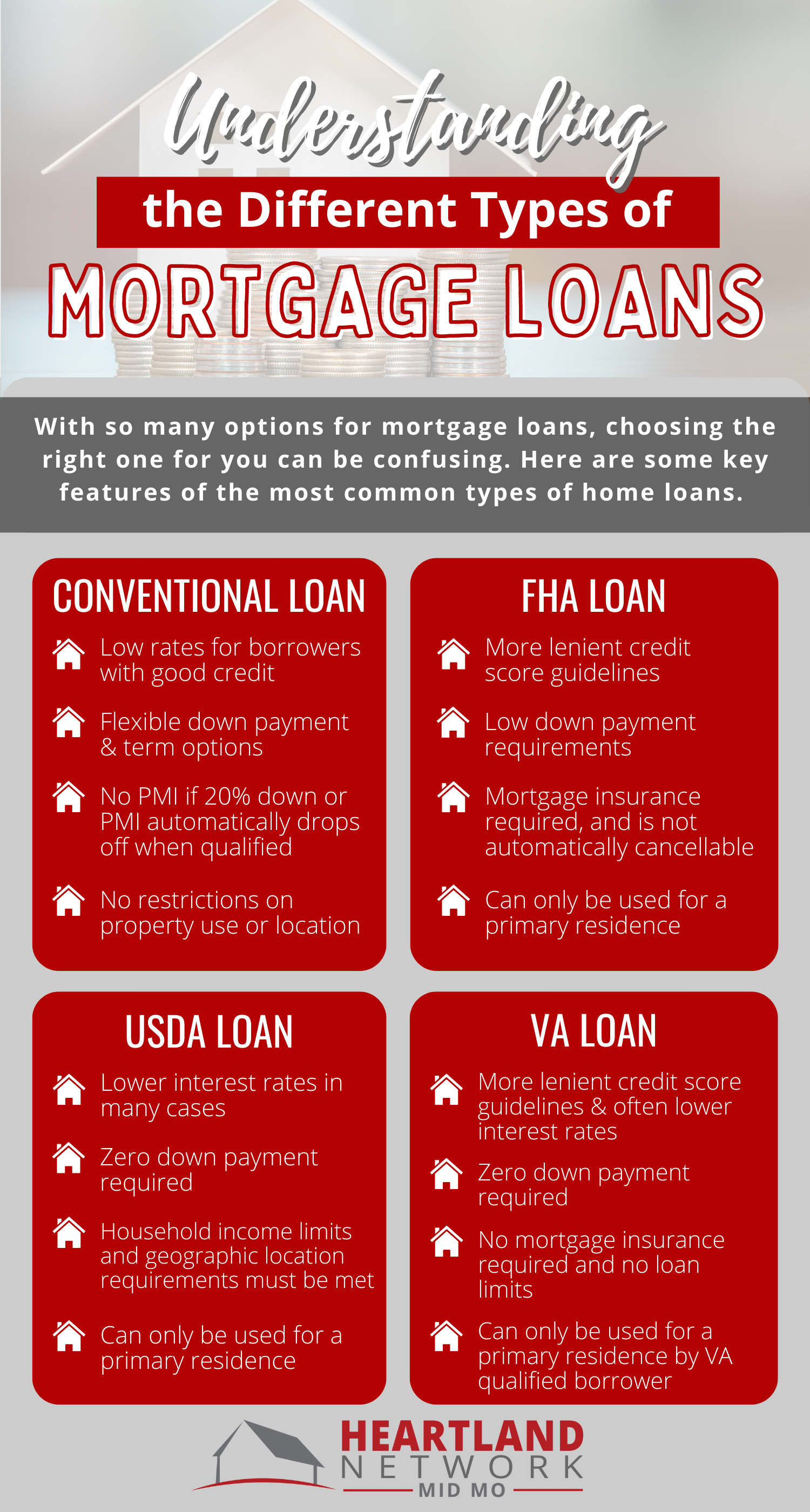

What is good Virtual assistant Financing?

An excellent Virtual assistant loan are supported installment/signature loans in my area by the us government and that’s discover to active and you may former services users as well as their thriving spouses in the some instances. You can fool around with a beneficial Va mortgage buying or make a great family, improve and resolve a home, or refinance a mortgage. Tall benefits tend to be less credit score standards, no individual mortgage insurance coverage, no down payment specifications, and you can aggressive cost.

You could apply for a great Virtual assistant mortgage over and over again, nevertheless money percentage develops while using the an effective Virtual assistant financing immediately after your first go out. The Va financial support percentage are a single-big date charge you pay should you get a beneficial Virtual assistant-protected mortgage to order or re-finance your residence. Oftentimes, you will have the possibility so you’re able to roll new Virtual assistant investment commission into the the loan. The typical financing fee range from.4% to three.60% of your amount borrowed.

You’ll need good COE, which you’ll get on the Va site, otherwise your lender can help you with this particular. To get this certificate, you will have to make services-related records, that are very different based on whether you’re towards productive obligations or a seasoned.

Carry out Virtual assistant Finance Vary by Lender?

The two head suggests an excellent Virtual assistant mortgage can vary a bit out-of financial to financial would be the speed as well as the minimal credit history. The new Va will not underwrite the mortgage; it includes a vow on loan providers which give you the loan system. The lenders dictate the fresh cost they’re going to give, while the other underwriting guidance they will certainly comply with, just like your credit rating and you can debt-to-income proportion.

Credit rating minimal requirements disagree slightly out of bank so you’re able to lender, with many purchasing 620 since their acknowledged minimal. Borrowing from the bank restrictions aren’t set from the You.S. Company out-of Experienced Situations. Brand new VA’s just borrowing demands is actually for the fresh new debtor is believed a satisfactory borrowing exposure by a lender.

The key benefits of a great Virtual assistant mortgage are exactly the same it does not matter and therefore lender you choose. The benefits of the application are not any down-payment specifications, zero PMI specifications, no prepayment punishment, having good Va investment percentage using place of the brand new PMI.

Brand new Virtual assistant provides what are called lowest property standards. They have been non-flexible items like structure faults, termite infestation, leaks, pness, and continuing settlement inside or nearby the foundation. If you’re suppliers engaged with consumers who provide a non-Va financing with the get can discuss the fresh fix costs of these items, the new Virtual assistant program requires these products to get fixed prior to it will provide the lender brand new approval in order to straight back the lender’s financial financing into borrower. You to throws strain on the provider to fix these problems primarily during the the rates once they wish to be capable promote their home towards buyer who gifts that have a Virtual assistant financing within pouch.